Non-dilutive Funding in a Nutshell

How to start a start up

12/26/202416 min read

Souce: h/t KRC https://krogersconsulting.com/leadership/non-dilutive-funding-in-a-nutshell/

Non-dilutive Funding in a Nutshell

As a startup founder, you have at least seven sources of non-dilutive funding to consider:

Bootstrapping – funding from your own pocket

Friends and family – cash from those who know and love you

Grants – from government or nonprofit foundations

Debt financing – which comes in a dizzying array of options

Crowdfunding – depends on the appeal of your story

Competing for funds – in pitch or accelerator competitions

Cash for fee arrangements – often a precursor to an equity raise

Considering and ranking these options during your initial planning to strengthen your overall funding strategy and enhance your freedom to operate your business!

Read Part I of my non-dilutive funding series here.

Read Part II of the non-dilutive funding series here.

What Is Non-Dilutive Funding? Part 1

December 9, 2024

| Business, Product Development

We receive lots of questions about how to start a company to commercialize a new therapy. Many of those questions are about money. Props to #JessieJ, but most of us will need some money to make the world dance with our great idea. Now that I’ve put that little tune into your head, let’s spend this month looking into non-dilutive funding sources, aka startup money that doesn’t dilute your business ownership. Part 1 covers bootstrapping, friends and family support, and grants. Part 2 will cover debt financing and alternate funding approaches.

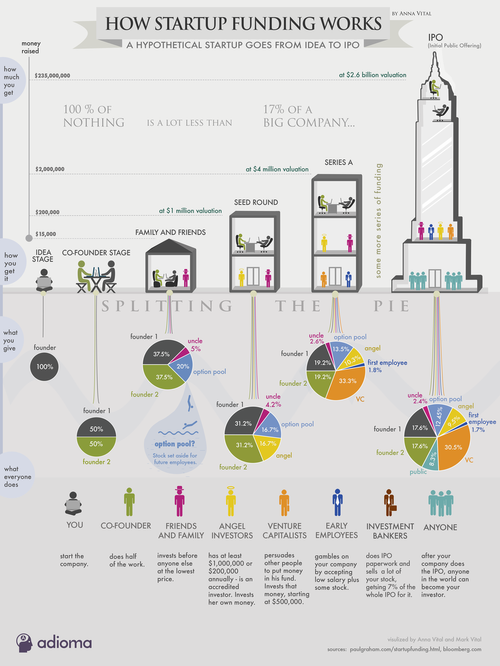

Adioma founder Anna Vital created this infographic on startup funding, which can help you orient yourself to the broader funding picture.[1]

Bootstrapping

When you create your startup, it may be just you, or you may have a co-founder or two. Many small companies start this way, and some become successful before accepting outside capital. The earliest sources of this capital will likely be family members or close friends who believe in you and your idea but prefer to contribute funds rather than effort. In this section, we’ll first review how bootstrapping works and look at the different phases.

Photo by MART PRODUCTION

How Bootstrapping Works

Bootstrapping means you start the business simply with very little money and no outside investments to pay your company’s expenses. A concise summary of the approach is this article by Ian Harvey.[2] Success in bootstrapping requires entrepreneurs to develop their skills (especially in business) and focus on achieving profitability. Without outside investors, a founder will have to rely on themselves (and any co-founders) to find, make, or buy everything needed. Bootstrapping is easier for serial entrepreneurs who have money from a previous company to invest in a new business. Still, it’s equally possible for new companies that don’t require a lot of capital to buy equipment, rent facilities, or pay employees. It’s cheap to start, and the founder makes all the decisions and concentrates on the business. Cash flow will be a problem until you find customers willing to pay, and the risk of failure can be high. If you have co-founders, there’s a risk of disharmony torpedoing the business, including disagreements over equity. Bootstrapping requires a fair amount of discipline, focus, and confidence, but success is entirely possible.

Bootstrapping’s Phases

There are three phases of growth for a bootstrapped business, and each potentially adds a different set of funding sources to the mix. The beginning stage is self-funded by the founder(s) through savings, borrowing on credit cards or lines of credit, and starting the business on the side (while keeping your day job). Anyone thinking about starting a business should start saving money and establishing an excellent credit rating as soon as possible. Self-funding is also enabled by keeping costs as low as possible, minimizing inventory, and protecting your IP. Once you are selling enough of your product or service to meet expenses, the business moves to the customer-funded stage, where the owner(s) reinvest profits to help the company grow. Companies that put a product or service on the market quickly, like apps or converting a physical service to virtual delivery, can reach and leverage the customer-funded stage in a short time period. The business reaches the credit stage when you need to fund specific activities for growth, like improving equipment or hiring staff. This stage involves external financing, such as a loan to support the expansion. Loans are easier to find when the business can demonstrate a revenue history. However, loans during this stage are more likely to be secured with personal assets. During all three stages, there may be subsidies that help you sustain the business, like tax reductions for companies below a certain amount of income or government cash payments that help you compete. [3]

Friends & Family Support

When bootstrapping isn’t quite enough, you may have friends or family wanting to back your idea. They may have funds to loan on reasonable terms or a percentage of the company’s future value. They may contribute professional skills or talents in the form of effort for a portion of the future proceeds (assuming you or they don’t want to join as co-founders). Developing your business skills and getting expert advice helps you structure these deals to avoid future disagreements and meet applicable regulations. The friends and family stage is often the point where business financing tips over into the dilutive phase. The difference is in the relationship you already have with the party interested in the business, which generally results in only a minor dilution of your ownership. Anna Vital notes that this may be an ideal point for establishing the equity structure against future deals, including an option pool for prospective employees.

Photo by airfocus on Unsplash

You and your new company need funds to operate as you bring that great idea to the market. Those funds can come from various sources, but most entrepreneurs start with their savings, credit, and other resources. Success at this stage also comes with founder effort, improved knowledge, and business skills. Once revenue increases beyond operating expenses, the excess can fund further growth or facilitate credit for capital investments. Your business may also benefit from the participation or funding of friends and family. A company can thrive in any of these stages for any length of time. However, businesses with a long lead time to market (like medicines, diagnostics, and medical devices) will likely need other non-dilutive funding to succeed, including grants.

Photo by George Chambers

Grant Funding

Grant funding is not shown on Anna Vital’s infographic, although it is a significant source of early capital for life-science and technology startups. Organizations with grant funds post a proposal request, and companies compete for a portion of the funds. The process, while time-consuming, can help clarify your idea and provide a significant amount of cash. Grants are often associated with post-secondary research and education institutions, but they are also available to small businesses. This section will review grant sources in the US, focusing on federal research and commercialization programs and foundation grants. We’ll also look at early capital and support resources available to small businesses in Canada.

Grants are one way to get cash to fund your business.

US Grants

The US government funds basic and applied research that meets federal priorities through grants from its many agencies. Small businesses are eligible for some of these grants, which you may find using the Search Grants tool. The National Institutes of Health are the primary source of these grants, although many other agencies use this mechanism. Each grant has specific requirements outlined in the Notice of Funding Opportunity (NOFO), and applicants should pay careful attention to these details in their applications. Familiarity with the research interests of the sponsoring agencies like NIH or DOE will also help align applications with agency needs. Interaction with agency scientists may also help entrepreneurs refine their ideas for submission. Check your state government website, too, as many states offer grants for areas of local investment. In Canada, research and development grant funding is available to businesses interested in collaborating with the National Research Council (NRC). Canadian entrepreneurs may also work with one of the fourteen NRC research centers, eight collaboration centers, or other R&D programs.

NIAID’s Dale and Betty Bumpers Vaccine Research Center, NIH campus, Bethesda, MD.

The primary commercialization grants for small businesses in the US are the Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs. [4] These grants are a mechanism for the US government to support small US-owned and based businesses with early starting capital to develop and commercialize ideas that meet federal needs. Both programs have criteria for the size and ownership of the funded company; STTR also requires a partnership with a US non-profit research center. Medical device entrepreneur Paul Reynolds shares an excellent overview of the SBIR program, application process, and potential outcomes in this post. [5] Some of his tips apply to research grant applications. Canada has a similar program funded through the NRC called IRAP.

Non-profit foundations have been a source of innovation funds since the 19th century. Still, their impact has increased significantly in the last three decades with the rise of patient-focused organizations dedicated to a specific disease (for example, the Cystic Fibrosis Foundation, the Michael J. Fox Foundation for Parkinson’s Disease, or one of my favorites, the National Organization for Rare Disorders. Other foundations focus on funding work towards specific goals. For example, the Gates Foundation focuses on global health, gender equality, and economic opportunity, while the X Prize sponsors competitions for “crazy ideas” across a range of significant problems. Incubators, investors, and industry advocacy groups are also in this space, offering cohorts, pitch competitions (see part 2), or fellowships. This type of support includes the networking and advisory connections essential to future funding opportunities. Foundations fund opportunities around the globe, too. I recommend you complete a search for non-profits related to your area (recruit your local public librarian for help) and keep track of at least the top three activities.

Grants represent another source of early capital for startups. They can be time-consuming to find, and the application and award process tedious and slow, but they offer benefits in networking and advice from experts, and cash payments. It would be best to consider whether and where grants fit into your business funding and development strategy. Some entrepreneurs stay with grants for an extended period of product or service development, while others skip the grant approach because its pace delays market launch.

Making strategic decisions about funding sources is one of the thrills and challenges of founding a startup. In part 1 of this series, we reviewed bootstrapping, friends and family, and grants as funding options. In part 2, we’ll discuss debt and alternative nondilutive funding.

Photo by Markus Winkler on Unsplash

Disclosure Notice: This article cites several funding sources. Neither the author nor Katrina Rogers Consulting has any financial interest in those sources nor recommends any particular one. We recommend you do your homework, understand your choices, and scrutinize all documents and agreements to understand them fully before signing.

References

[1] Anna Vital, How Funding Works Infographic. Accessed October 11, 2024. https://annavital.com

[2] Ian Harvey, “Companies that Succeeded with Bootstrapping: How entrepreneurs bootstrap their companies to success.” Investopedia.com, updated August 21, 2024. Accessed October 11, 2024. https://www.investopedia.com/articles/investing/082814/companies-succeeded-bootstrapping.asp

[3] Investopedia, “Subsidies: Definition, How They Work, Pros and Cons.” Investopedia.com, updated February 28, 2024. Accessed October 11, 2024. https://www.investopedia.com/terms/s/subsidy.asp

[4] “About SBIR and STTR” website, https://www.sbir.gov/about. Accessed October 11, 2024. https://www.sbir.gov/about

[5] Paul Reynolds, “Small Business Innovation Research (SBIR) | Non-Dilutive Funding for Your Company.” IEEE Enterpreneurship, May 8, 2020. Accessed October 11, 2024. https://entrepreneurship.ieee.org/2020_05_08_SBIR-non-dilutive-funding/

PART 2

What Is Non-Dilutive Funding? Part 2

December 16, 2024

| Business, Leadership

We are discussing sources of non-dilutive funding this month. Simply put, non-dilutive funding is startup money that doesn’t dilute your ownership of the business. Part 1 covered bootstrapping, friends and family support, and grants. This part covers debt financing and alternate funding approaches. I hope you are enjoying this mini-series!

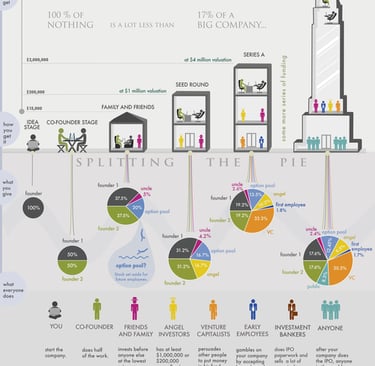

Adioma founder Anna Vital created this infographic on startup funding, which can help you orient yourself to the broader funding picture.[1]

In Part 1 of this series, we covered bootstrapping, friends and family, and grants as funding options. These are the options most people think about when they hear non-dilutive funding. Let’s now dig into some other funding options that don’t decrease your percentage ownership of your startup.

Financing Through Debt

Many founders decide they need outside money to sustain or expand their business. At that point, most are considering whether to choose between business debt or equity fundraising (selling shares of your company to outside investors). We touched on personal loans during part 1. We’ll discuss equity finance in next month’s two-part series on dilutive funding. In this section, we’ll help you understand debt financing, sort through the different sources, and examine the strengths and weaknesses of the approach.

A bank is not the only place to find debt funding for your business.

What is Debt Financing

Simply put, debt financing is borrowing a sum of money for your business that you will have to pay back in time with some amount of interest. The debt can be short-term (lasting no more than a year) or long-term (more than one year). Secured debt is backed by collateral or physical property that the lender can take if the business defaults on a loan (the mortgage on a house is a good example). Unsecured debt is based on the promise of repayment by the borrower to the lender, and therefore carries higher risk and a higher interest rate. A founder’s ability to access debt financing is directly proportional to their credit rating. It is an excellent reason to get your personal accounts in good shape before you launch that startup. With any debt, you should only borrow what you need and have a clear plan for using those funds. Establishing this discipline at the start makes your business a better bet for future lending.

Debt Financing Sources

Debt financing comes from several sources.

The first and simplest is managing your accounts payable or making payments to your suppliers at the last possible minute. Many founders use this approach, intentionally or not, but it requires a careful eye on the due dates. Miss a few payment deadlines, and your vendors may cut you off or increase your requirements.

Personal debt on credit cards is generally considered bootstrapping, but I’ve also seen it classed as debt financing, most obviously because it is debt. Interest rates are typically consistent with what an early-stage company can expect to pay (10-30%), and credit cards are often easier to obtain than loans.

The US Small Business Administration helps companies secure loans from traditional lenders through various programs. The SBA provides funds or guarantees to the lenders who then originate and administer the loan(s). Traditional banks often have high revenue and credit rating requirements to deliver business debt services like term loans, credit lines, and merchant cash advances. Companies with slightly higher revenue and a good credit rating can access those services from specialized vendors. Online examples include Kabbage, FundingCircle, or LoanBuilder.

Community development financial institutions (CDFIs) are privately owned financial institutions that provide affordable loans to businesses founded by low-income, low-wealth, and other disadvantaged people. CDFIs (like Craft3 in the Pacific Northwest) offer founders and owners access to creative and affordable financing for up to 100% of their projects.

Venture debt is loans provided to companies based on their future financing rounds and is very popular in Tech businesses. Shoring up your cash position to delay financing or fund certain capital investments can be beneficial, especially when those extra few months get you to a better place for an equity fundraising round. A great explanation of venture debt is in this 2011 post by VC Fred Wilson.[1] Venture debt often occurs as a bridge loan from an existing investor to move the company to its next level of profitability.

Revenue-based financing is a loan where the lenders (usually investors) receive a percentage of the business revenue. There is not a fixed monthyly payment; instead, the payment is a percentage of your cash receipt. The total amount repaid is the initial investment (loan) times the repayment cap (a number between 0.4 and 2.0). This financing can be good for businesses with stable revenue and reasonable monthly expenses. They can be more expensive than traditional loans. Olivia Chen of NerdWallet gives an excellent overview of revenue-based financing in this post.[2]

Pros and Cons of Debt Financing

As in any financial strategy, debt financing has its pros and cons. The pros include securing your ownership and retaining management control of strategy and goals. Once the debt is paid, your liability is over. You don’t have to share the rest of your profits with the lender. The interest payments on business debt are a tax-deductible expense, shielding some of your income. That’s a significant advantage when that income is still low. The interest rates for debt, while they seem high, are less than the cost of equity due to the tax deduction on interest payments. Debt financing is more accessible to most businesses, and careful use of debt can enhance your business’s credit score. The cons of debt financing include paying it back per the agreed schedule, regardless of how you are doing. Debt will necessarily reduce your cash flow because of the principal and interest payments. It requires care in separating your business and home accounts to keep your personal assets secure if you must default. Your lender may also require personal assets as collateral, which places them at risk. When you choose variable interest rates or lines of credit, the financing terms can change over time. Too much debt can negatively affect your business credit rating and future valuations if you later seek funding in the market.

Do Your Homework

Debt financing can be complex, and each business has an optimal set of scenarios. I recommend finding trustworthy advisors to help you assess your options. Research is useful to help you learn the language and options. Here are some articles I found helpful. Mesh Lakhani is spot on in advising us that, while the fundamentals are sounds, markets change.[3]

Alex Gold, “Telltale Signs That You Shouldn’t Be Raising Venture Capital,” Entrepreneur.com, January 24, 2020.

Rosemary Carlson, “Pros and Cons of Debt Financing for Small Business Owners,” The Balance Small Business, March 19, 2021.

Mesh Lakhani, “A Founder’s Guideline to Debt Financing,” Startup Grind, April 10, 2018.

Alternate Funding Approaches

Where do you turn when you have maxed out your credit cards, emptied your bank account, tapped out your friends and family, don’t want to get into the grant cycle, and aren’t quite ready for debt financing? There are still three options to consider while planning your funding strategy. If your idea has social media appeal, you can try crowdfunding. Pitch competitions offer cash payments and other forms of support to the winning company. If you have a small amount of revenue, you can leverage it for immediate funds and an entry path into additional dilutive funding (the topic of our next blog series). In this section, we’ll take a closer look at these approaches.

You may have to take advantage of different funding options to keep building your startup .

Crowdfunding

Crowdfunding is a way to raise money from large numbers of individuals to fund your business.[4] Crowdfunding platforms manage the process, facilitating the entrepreneur’s pitch to investors, who can invest their money in the project. Some projects are altruistic, with no return to the investor other than goodwill, and some are rewards-based, offering an advance copy of the product or a small amount of equity to the investor. Different platforms have rules for the projects they fund, and all generate revenue by taking a percentage of the funds raised for the project. In addition to raising funds, crowdfunding lets a business grow its audience, interact with customers, and assess public opinion. Disadvantages include the platform fee (which ranges from 5-12%), the rules of the platform (some don’t pay unless you reach your funding goal), and a market attitude that companies that “resort” to crowdfunding are unworthy of investment. Nevertheless, many commercial companies have raised money via crowdfunding. Regulation rowdfunding is a type of security regulated by the SEC and a form of equity fundraising.[5]

Competing for Funds

Pitch and investor competitions are a thrilling approach to raising funds. All across the US, incubators, investment funds, universities, and companies sponsor competitions where entrepreneurs can pitch their ideas for a prize. The prize is usually cash but may also include other support such as business and advisory services, mentoring, or residency in a startup space. Finalists may be eligible for funds to attend the final competition. Global examples include JLABs QuickFire Challenges in the biomedical area, Pegasus Tech Ventures Startup World Cup on tech to improve lives and transform industries, and SeedStars World Competition with a broad industry focus. Look first in your local business and entrepreneur community, as smaller-scale competitions are everywhere (like the pitch competition at Flywheel Investment Conference in Washington state, where startups compete for a $150,000 convertible note and a $50,000 relocation award to move into central Washington). There are so many competitions you can comfortably attend one in advance to evaluate the experience. An additional benefit of competing is the chance to practice and refine your pitch in front of seasoned investors and see how others manage their pitches. This kind of experience is invaluable no matter which funding strategy you use.

Photo by Product School on Unsplash

Cash for Fee Arrangements

Cash for fee options often precede an equity raise. If your revenue is positive but too low to secure debt financing, you can use some creative options to obtain cash upfront for a fee. Companies like Capchase, Founderpath, and Pipe offer companies loans based on monthly, quarterly, or annual recurring revenue (ARR).[6] The loan amount is for the ARR minus a discount rate (the fee), and the company pays back the loan over the year at the total amount. For example, a company with $120,000 ARR and a discount rate of 10% can receive an up-front amount of 108,000 and pay back 120,000, which covers the discount rate. Popular with SaaS companies, ARR as a lump sum can fund any tech company with regular recurring revenue. Its scalability and ease of use make it a rapidly growing source of funds for companies with recurring revenue.

If you are planning to raise funds from investors in the future, shared earning agreements (known as SEALs) are a way to enter that market on a small scale.[7] These agreements provide cash upfront for a company with low recurring revenue (<$50,000) in exchange for a small stake (the fee). The company can buy back two-thirds of that stake over time. The deal turns into a simple agreement for future equity (called a SAFE) if the company pursues additional funding rounds. Tiny seed funds also fill a funding gap for very early-stage companies that are successful on a small scale.

The Take Home Message

As a founder, you will be challenged to select the best mix of funding for your business. Different funding sources are appropriate for different business stages and levels of risk tolerance, and only you can make those decisions for your business. It’s essential to recognize that you have many options. Debt funding can help you manage your capital while preserving your equity and control in the company. Options are available for additional funding even when you think you have exhausted all your options. All will require you to get a little outside of your comfort zone, whether it is going the social route with crowdfunding, pitching to investors live during intense competitions, or investigating ways to leverage your current revenue stream. Considering and ranking these options during your initial planning will strengthen your overall funding strategy and enhance your freedom to operate your business.

Disclosure Notice: This article cites several funding sources. Neither the author nor Katrina Rogers Consulting has any financial interest in those sources nor recommends any particular one. We recommend you do your homework, understand your choices, and scrutinize all documents and agreements to understand them fully before signing.

Read Part I of this series.

Funding your startup can sometimes be a struggle.

References

[1] Fred Wilson, “Financings Options: Venture Debt.” AVC.com, Accessed October 11, 2024. https://avc.com/2011/07/financings-options-venture-debt/

[2] Olivia Chen, “ What is Revenue-Based Financing?” Nerdwallet.com, June 16, 2023. Accessed October 11, 2024. https://www.nerdwallet.com/article/small-business/revenue-based-financing

[3] Mesh Lakhani, update to “A Founder’s Guideline to Debt Financing,” Startup Grind, April 10, 2018. Accessed October 11, 2024. https://medium.com/startup-grind/a-founders-guideline-to-debt-financing-14e99e9d58b6

[4] Tim Smith, “Crowdfunding: What it Is, How It Works, and Popular Websites.” Investopedia.com, updated May 30, 2024. Accessed October 11, 2024. https://www.investopedia.com/terms/c/crowdfunding.asp

[5] U.S. Securities and Exchange Commission, “Regulation Crowdfunding” website. Accessed October 11, 2024. https://www.sec.gov/resources-small-businesses/exempt-offerings/regulation-crowdfunding

[6] Chris Metinko, “Got Revenue? Atlernative Financing Tools Look to Help SaaS Founders Avoid Dilution.” Crunchbase.com, February 11, 2021. Accessed October 11, 2024. https://news.crunchbase.com/venture/got-revenue-alternative-financing-tools-look-to-help-saas-founders-avoid-dilution/

[7] Chris Metinko, “Too Small for Venture? SEALs and Early-Stage Investment Firms Offer Financing, Although Options are Still Limited.” Crunchbase.com, March 11, 2021. Accessed October 11, 2024. https://news.crunchbase.com/startups/too-small-for-venture-seals-and-early-stage-investment-firms-offer-financing-although-options-still-limited/

Innovation

Pioneering advancements in biotechnology for developing new drugs. Providing low cost custom formulations, generic and off patent drugs for repurposing in rare and orphan diseases.

Research

Sign Up for updates

Generic finished formulations

Oncology drugs in development

© 2024. All rights reserved.